Payment fraud incidents have been on the rise, increasing 88% since December 2021, PYMNTS Intelligence research reveals. For instance, 11% of consumers who paid for groceries experienced payment fraud in March 2023, compared to 5.7% in December 2021.

Amid this surge in fraud incidents, consumer fears of data breaches and vulnerability to fraud are fostering reluctance towards apps aggregating and connecting payment information. This concern spans various demographics, including generation, education, income and financial lifestyle, as highlighted in the study.

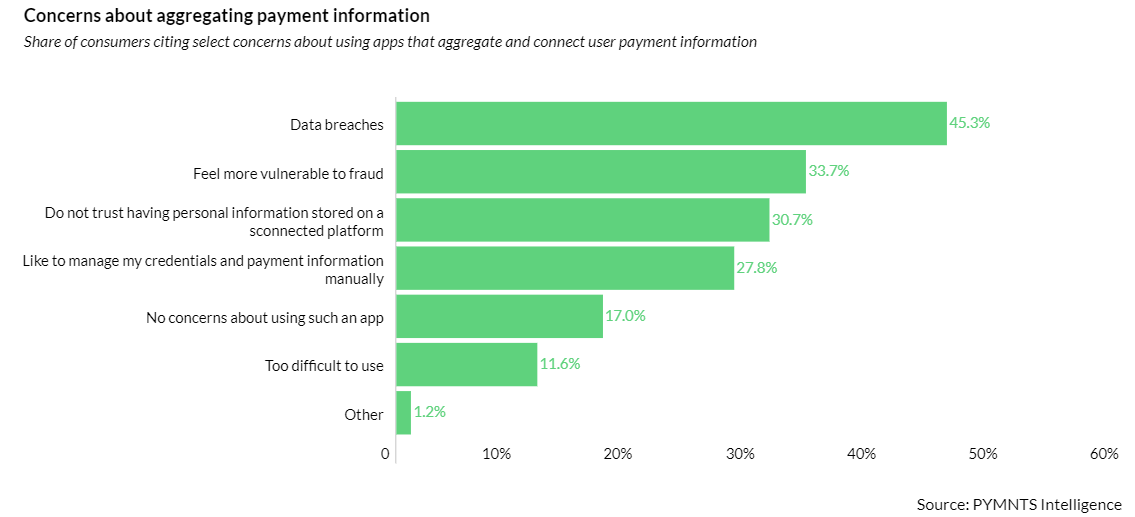

Specifically, 45% of consumers are afraid of data breaches, and 34% feel more vulnerable to fraud. Additionally, about 30% do not trust having their personal information stored on a connected platform, while 27% would prefer to manage their credential and payment information manually to minimize risks.

Fear of fraud or data theft also remains a top concern for consumers when making online bank transfers. In fact, with over 70% expressing at least slight concern about security in this context, it becomes crucial for banks and businesses to proactively address this challenge. This includes continuously enhancing measures to protect customer accounts and transfers from fraud, while also effectively communicating security protocols to reassure customers and alleviate their fears.

The increasing sophistication of fraud has resulted in customer losses for firms, with 34% of surveyed FinTech and Big Tech companies reporting such impacts. Moreover, over 25% of these firms admit that existing solutions struggle to identify fraudulent transactions, while 31% highlight ongoing challenges related to cyber and data breaches in the fight against fraud.

FIs Up Cyberdefenses With AI

The repercussions of fraud sophistication extend to financial institutions (FIs) as well. According to a collaborative study by PYMNTS Intelligence and Hawk AI, nearly 43% of FIs in the U.S. witnessed an uptick in fraud cases between 2022 and 2023. This translates to a 65% increase in fraud losses, from $2.3 million in 2022 to $3.8 million in 2023.

These alarming numbers indicate that existing measures are not keeping pace with evolving fraud schemes, and firms must enhance their preventive measures to address this growing concern.

For FIs, this has meant increasingly deploying artificial intelligence (AI) and machine learning (ML) to build robust cyberdefense strategies. In 2023, nearly 70% of FIs with assets over $5 billion leveraged ML or AI solutions, marking a significant increase from 34% in 2022.

And the investment in AI solutions appears to be yielding positive results. The study shows that adoption of AI solutions has led to a notable decline in overall fraud rates, highlighting the effectiveness of this technology in preventing fraud.

Importantly, this technology doesn’t need to be confined to the fraud or payments space. As Erika Dietrich, vice president, global fraud prevention risk services at ACI Worldwide, highlighted in an interview with PYMNTS, “once you’ve upscaled your technology stack and gotten your technical colleagues aware of how to use AI technology and apply it, it can be applied to use cases beyond just fraud or payments. It’s about applying this innovation across your business organization in a multitude of different ways.”

"payment" - Google News

January 25, 2024 at 08:02AM

https://ift.tt/xLGZfrK

Fraud Concerns Leave Consumers Skeptical of Payment Apps - PYMNTS.com

"payment" - Google News

https://ift.tt/7VhfXrm

https://ift.tt/kIyn4jW

Bagikan Berita Ini

0 Response to "Fraud Concerns Leave Consumers Skeptical of Payment Apps - PYMNTS.com"

Post a Comment