Nearly nine in ten Americans are now using some form of digital payments, and they are engaging with these rapidly evolving solutions in an increasing variety of ways. These are among the key findings of McKinsey’s 2022 Digital Payments Consumer Survey, the seventh in an annual effort that reveals continued growth as well as subtler shifts in consumer preference and behavior.

While the continued mainstreaming of digital payments is hardly a surprise, the manner in which consumers are incorporating the service into their financial lives provides valuable insights for providers aiming to extend or establish retail relationships. Our August survey of more than 1,800 US consumers also provides new details on behavior surrounding two high-profile payment vehicles: buy now, pay later (BNPL) financing and cryptocurrency.

The wallet’s digital renaissance

Not only has digital-payments penetration increased to 89 percent in 2022, but the share of respondents who report using two or more forms of digital payments has grown even more rapidly—from 51 percent in 2021 to 62 percent. In-app and peer-to-peer (P2P) purchases exhibit the greatest gains, in many cases building upon existing use of online payments (still the leading digital use case, used by 69 percent of consumers).

More than two-thirds of Americans expect to have a digital wallet within two years, and it’s likely that many will hold multiple wallets. Our 2022 survey revealed a marked increase in the share of consumers intending to use three or more digital wallets in the coming years: from 18 percent in 2021 to 30 percent in 2022. This is a notable change from the legacy model of carrying around a single leather wallet.

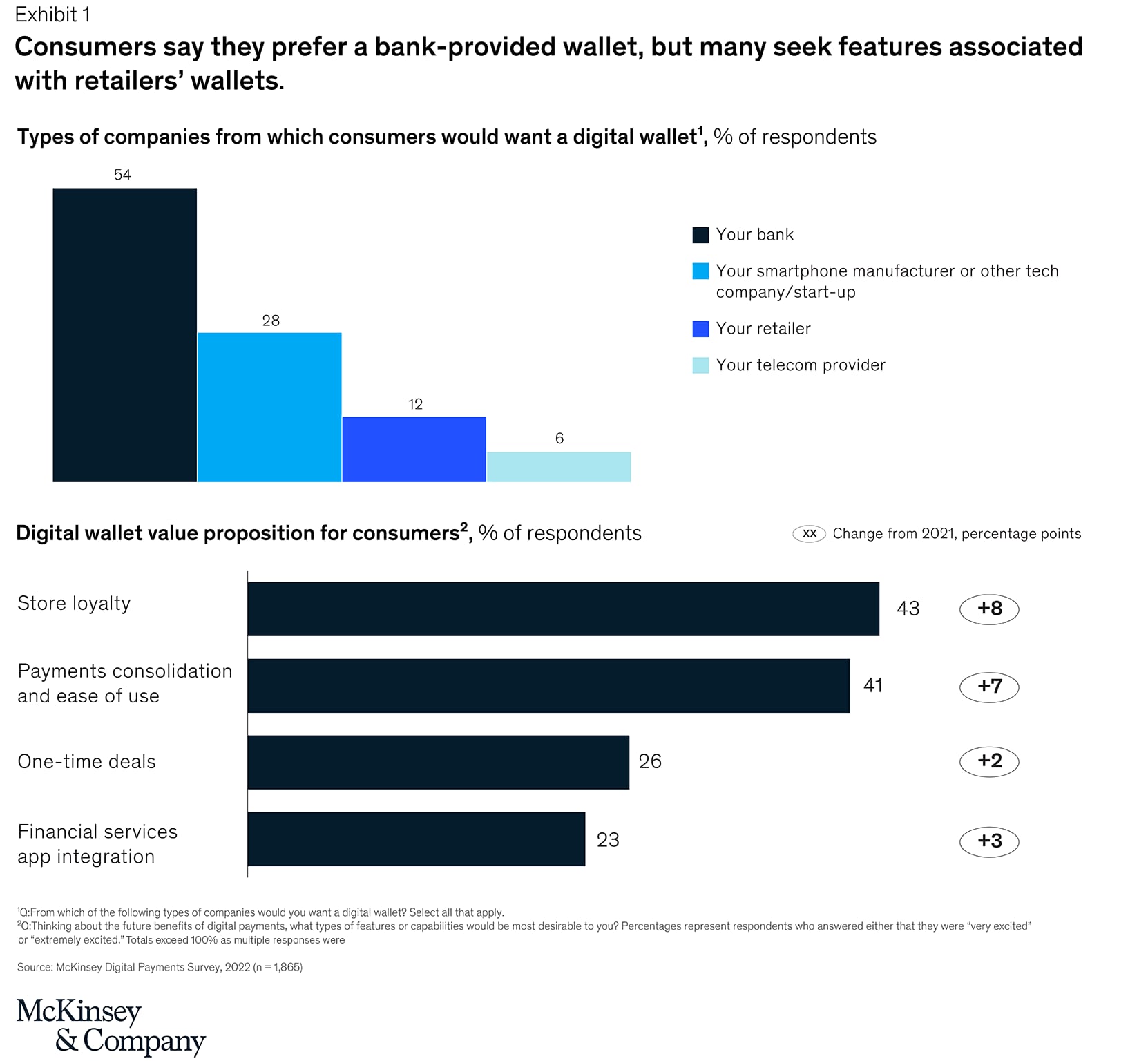

When asked who they consider the logical provider of digital wallets, consumers in all age groups and by a wide margin identify their bank, with the runner-up being a smartphone manufacturer and/or tech company (Exhibit 1). These survey results, however, don’t seem to match consumers’ descriptions of their actual behavior; respondents are far likelier to say they use digital wallets from PayPal, Apple Pay, and Google Pay (across both online and in-person channels) than to identify any other providers. In light of this disconnect, banks would be wise not to rely on existing customer relationships but instead identify paths to deliver on the stated consumer requirements.

In terms of wallet selection criteria, consumers—again consistently across age groups—seek not only payments functionality but also the integration of loyalty/rewards capabilities, as well as solutions offering a broad range of financial services and compatibility with their existing apps. Preferences for the types of financial services included (for example, loans, credit and debit cards, and wealth management) were relatively evenly distributed, indicating a market opportunity for a financial institution capable of delivering a robust multifunction wallet. The first movers on this front are nonbanks—for example, PayPal’s wallet, with its integration of “pay later” BNPL functionality, and Block’s acquisition of Afterpay to augment its Square Cash offering.

BNPL behaviors revolve around card trends

Perhaps surprisingly, our survey did not reveal an increase since 2021 in the share of US consumers currently using BNPL services (30 percent in 2021 vs 28 percent in 2022). However, the share of respondents reporting interest in future use did increase from 11 percent in 2021 to 15 percent in 2022. The products for which BNPL is used are changing slightly, but small-ticket categories such as apparel and mid-ticket items, including electronics and home appliances, continue to lead.

Consumers’ reported buying behavior supports the idea that BNPL can deliver incremental sales growth, consistent with the results in 2021. Across all categories in 2021 and 2022, more than one-quarter of users reported they would either have bought less or not made the purchase had a BNPL option not been available. This impact was strongest in the category of mattresses and furniture, where the BNPL option increased sales by eight percentage points, and in solar power installation, where BNPL boosted sales by four percentage points. Among those who say they would have proceeded with their purchase without the BNPL option, 57 percent indicated they would have used a credit card, while the remainder cite debit cards or—a distant third—cash.

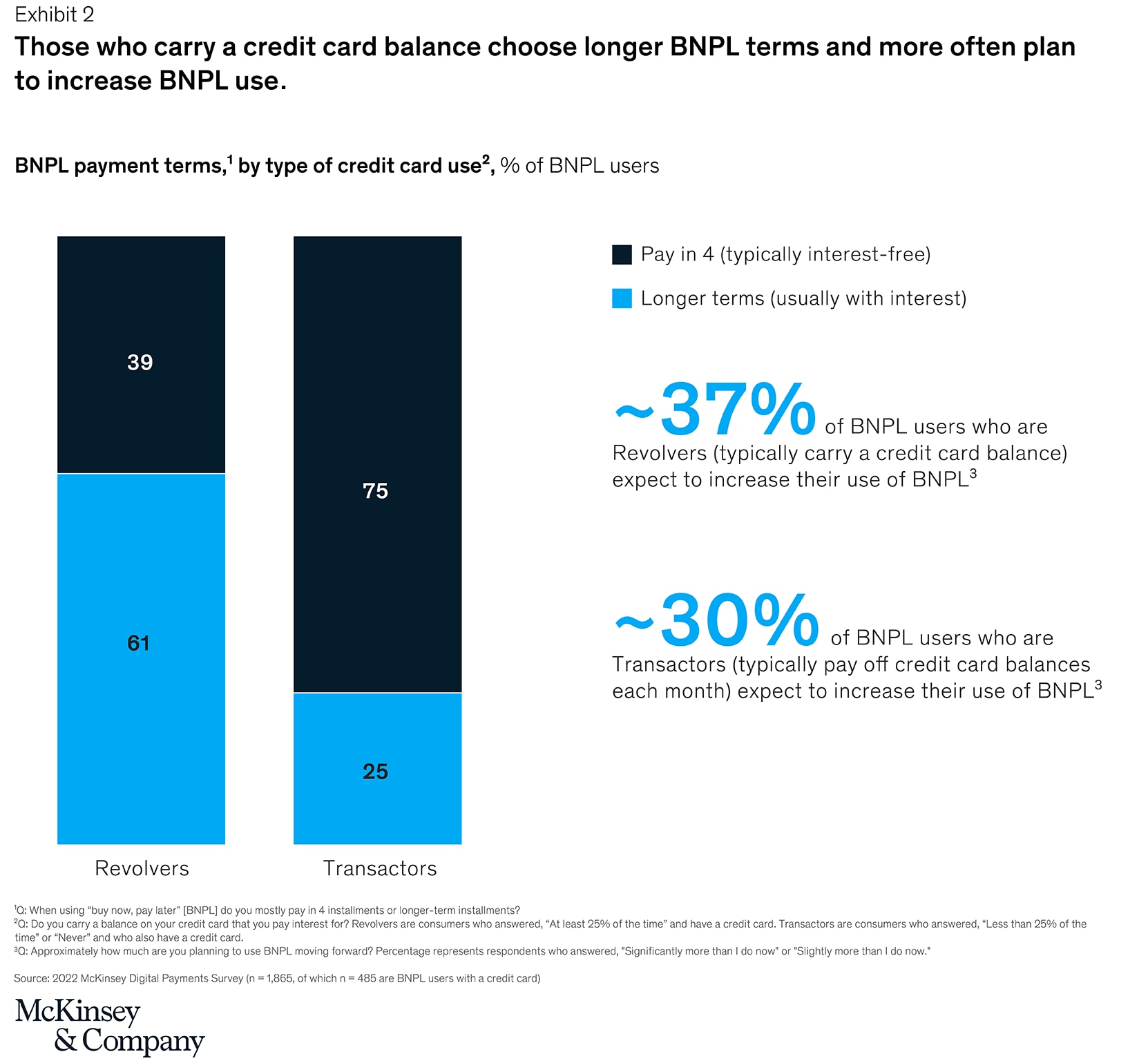

Further insight comes from a closer look at the BNPL cohort otherwise inclined to use credit cards. We categorized these survey respondents according to their reported usage patterns: 29 percent say they tend to pay their balance in full each month (known as Transactors), while the other 71 percent (designated Revolvers) say they carry a credit card balance from month to month. The survey sample skews significantly more toward Revolvers than the general US population, with striking behavioral differences between the two cohorts. Three-quarters of Transactors say they usually opt for the typically interest-free “pay in 4” repayment schedule (as opposed to longer terms, which often involve interest charges), whereas only two-fifths of Revolvers opt for “pay in 4” (Exhibit 2). This implies that Transactors, who are accustomed to avoiding interest charges on their credit card balances, also prefer interest-free BNPL products. Further, Revolvers more often indicate that they intend to increase their use of BNPL.

Relative stability through the crypto winter

The drop in cryptocurrency values since last November’s high-water mark corresponded with a halt in the meteoric rise of crypto ownership, which more than tripled from 2020 to 2021. Crypto penetration held steady in 2022, in terms of both actual ownership (15 percent, which represents a slight uptick) and those expressing an interest in owning (14 percent).

Among the roughly two-thirds of survey respondents expressing no interest in crypto ownership, their stated objections differ from responses in our previous surveys. An increasing share (39 percent) cites volatility as a barrier. Trust factors—in terms of both technology and counterparties—also are mentioned more frequently. In addition, more respondents than last year cite concerns with crypto’s long-term viability and the lack of a support channel should things go wrong.

Among those who do own crypto, nearly three-fifths hold less than 5 percent of their savings in these assets. On the other end of the spectrum, fewer than one in six respondents have committed more than 20 percent of their savings, and just 4 percent have more than half of their savings in crypto.

As economic conditions change, consumer spending habits and the payments channels they use tend to evolve. Today, perhaps because of overall economic uncertainty; certain stated consumer preferences seem at odds with evidence from the market. However, for digital-payments providers, the survey results provide some clear markers for building a digital product that appeals to consumers.

Copyright © McKinsey & Company. All rights reserved.

"payment" - Google News

October 22, 2022 at 01:13PM

https://ift.tt/ZDH4Ttr

Consumer trends in digital payments - McKinsey

"payment" - Google News

https://ift.tt/ChUX7Rl

https://ift.tt/VsCIcWj

Bagikan Berita Ini

0 Response to "Consumer trends in digital payments - McKinsey"

Post a Comment